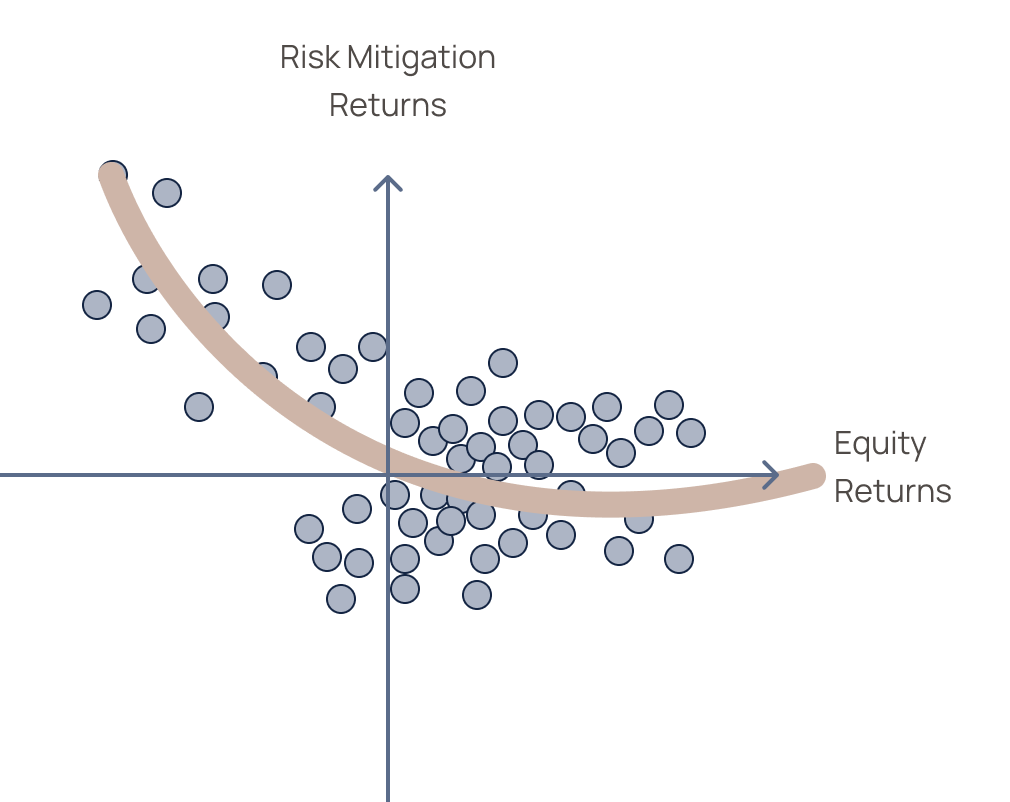

1. Maintaining a consistent negative correlation to equity markets

2. Increasing downside protection during periods of market stress

3. Generating positive alpha over time versus a passive short-equity exposure

4. Operating within a strict and transparent risk management framework